VC firms betting more on smaller seed investments than Series A: GSF Survey

Venture capital firms are sewing more deals in smaller-ticket, seed-stage investment space in India, compared to betting relatively larger sums in Series A rounds, according to a GSF Superangels survey that focused on early-stage investments in the country.

GSF Superangels was founded by former Reliance Entertainment president Rajesh Sawhney, who also started GSF Accelerator, a startup accelerator programme, in 2012.

GSF surveyed some 40 VCs and angel investors and found that the overall mood was one of caution, with the VCs making multiple smaller bets, and several erstwhile active angels skipping fresh bets in 2012. Here is a look at the key points of the report.

Investment volume & collaboration

More than 75 per cent of the VCs made less than 10 investments in India and over 40 per cent of them made fewer than five investments. Similarly, more than 50 per cent of the angels only made up to five investments. This is in line with the conventional spread of investments for a typical VC or angel investor in any given year in India.

However, the most interesting aspect is that both these early-stage investors have bet across 'stages' – thus breaking the traditional norm of angels coming before VCs. A lot of collaborations or co-investments, in which angels and VCs invested together, were also seen, with 61 per cent of the angels surveyed mentioning that there was greater collaboration in 2012, compared to the year before.

According to the survey, the collaboration will keep increasing as VCs continue to move down the 'value chain' of investing, indicating the emergence of a new hybrid investment paradigm for early-stage funding. VCs will develop strong partnerships with select angels and participate in their deals, thus gaining low-risk exposure to multiple industries without the cost of intensive diligence, while angels will gain by developing high quality exit options.

Another interesting phenomenon that goes in line with the Series A crunch in India, as also globally, is that of growing participation of VCs in seed rounds. In fact, there were more seed-level participations than Series A ones by VCs, with 42 per cent of the VC deals being seed investments in comparison, as against 36 per cent of Series A investments. On the other hand, 79 per cent of the angel deals were seed investments, according to GSF Superangels.

Lack of exits

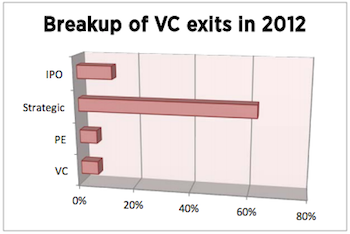

One of the biggest concerns of VCs and angels alike is the lack of exits/insufficient exit options. Angels saw very few exits in 2012, pointing again to caution on part of VCs with more of them choosing to 'wait and watch.' VCs, too, felt exits were highly constrained, with strategic divestments forming the bulk (over 60 per cent) of their exits in 2012 while IPO's constituted only 10 per cent. The report mentions that this lull will continue in 2013, with strategic exits accounting for the vast majority, despite sub-optimal returns.

One of the biggest concerns of VCs and angels alike is the lack of exits/insufficient exit options. Angels saw very few exits in 2012, pointing again to caution on part of VCs with more of them choosing to 'wait and watch.' VCs, too, felt exits were highly constrained, with strategic divestments forming the bulk (over 60 per cent) of their exits in 2012 while IPO's constituted only 10 per cent. The report mentions that this lull will continue in 2013, with strategic exits accounting for the vast majority, despite sub-optimal returns.

What's in store for 2013?

As of now, investors are wary of e-commerce (not surprisingly) and are waiting for the industry to stabilise. The only exceptions to this general outlook are seed funds that are extremely bullish and are contributing a significant chunk of early-stage investments in India. New angel investors will provide fresh capital to early-stage startups while seasoned ones are becoming wary. A few nascent seed funds will also make aggressive bets in 2013.

(Edited by Sanghamitra Mandal)

Next Article